March 24, 2026

We’re back.

After a period of building and refining the framework, MIQ Weekly is relaunching—with a sharper focus on regime, data, and cross-asset signals.

This first edition focuses on a critical shift now driving markets: the oil/ energy shock due to Hormuz block and the Middle East conflicts.

1. The Big Picture in Four Lines

Going into 2026, markets were firmly in a disinflationary growth regime, most clearly reflected in bonds. Growth was relatively stable, inflation was cooling, and the focus was on elevated real yields, tight financial conditions, and how these dynamics would interact with large-scale AI capex.

However, this growth was increasingly supported by household dissaving rather than income, making it more sensitive to tighter financial conditions and rising energy costs.

That regime shifted abruptly following the Israeli strike on Iran, pushing energy markets to the center of the macro narrative.

The key question is whether this becomes a sustained supply shock—and whether central banks choose to ease into it or remain restrictive—as this will determine whether growth stabilizes or weakens into recession and ultimately shape risk assets.

Key facts regarding the energy shock:

- Oil briefly surged toward $118 per barrel, now it is at 119 (data as of March 19th, European Morning).

- ~20% of global oil supply passes through the Strait of Hormuz.

- Strategic reserves could cover only 2–3 weeks of disruption.

- There are increasing indications that escort strategies in Hormuz would not be effective.

- The attack on key LNG infrastructure, particularly Ras Laffan and the South Pars/North Field complex, raises risks to global energy supply. Qatar accounts for roughly 20% of global LNG exports, making any disruption significant. Natural gas is a core input for ammonia (nitrogen fertilizers), so supply disruptions could push fertilizer costs higher and feed into food inflation.

- At the same time, Trump stepped back from immediate military escalation (March 24), signaling a temporary pause. However, Iran has denied any negotiations, framing U.S. statements as an attempt to influence energy and financial markets.

2. Growth Pulse

US macro data prior to the escalation showed resilience beneath the surface.

Manufacturing returned to expansion, consumer spending remained solid (though softening), and business investment—particularly in AI infrastructure—continued to support GDP growth (see Chart 1).

Consumption is no longer primarily driven by rising wages but by household dissaving (see chart 2). Wages are no longer rising and have been cooling since last year (see chart 3).

At the same time, interest-sensitive sectors remain weak. Spending has shifted toward non-cyclical categories based on the EBP research .

Dissaving, while supporting short-term consumption, implies reduced financial buffers and increased vulnerability to shocks—especially if interest rates tighten further or if consumers face sustained increases in energy prices.

In addition, dissaving tends to go hand in hand with increases in the wealth-to-disposable-income ratio, as illustrated by the Fourteen Research (see chart 4). This helps show that household wealth is closely tied to interest rates and that dissaving is not inherently bad for the economy.

At the same time, labor market data has begun to soften:

- January payrolls: +130k (vs +70k expected)

- February payrolls: -98k (vs +56k expected)

Higher energy prices now threaten this fragile equilibrium by compressing household purchasing power and corporate margins.

An energy shock would also impact both consumption and business activity through tighter financial conditions, reducing the ability to sustain dissaving.

Growth Snapshot:

- Payrolls: weakening

- Manufacturing PMI: 52.6 (expansion)

- Spending: slowing (2.4% vs 2.9%)

- GDP: 1.4% (distorted by shutdown effects – contraction in government spending)

3. Inflation Pulse

Inflation was clearly trending lower prior to the geopolitical escalation, with inflation swaps declining (see Chart 5 & 6).

One key reason lies in the composition of demand. Consumption has increasingly been supported by dissaving rather than wage growth, which produces a weaker inflation impulse than a wage-driven cycle.

Post-COVID, strong wage growth drove consumption. However, as wage growth slowed from Q2 last year, inflation dynamics began to shift (see Chart). While inflation picked up slightly into mid-2025, this is no longer driven by wages. However, the broader trend remained disinflationary.

This created a regime where:

- Growth held up

- Inflation eased

- Financial conditions remained tight

The energy shock now threatens to reverse that dynamic.

Oil briefly surged toward $118 per barrel. While prices have cooled, now it is trading above $100 again. Around 17 million barrels per day trapped in Hormuz (see chart 7),and the risk of sustained disruption through the Strait of Hormuz remains.

According to the Financial Times, the G7 is considering releasing 300–400 million barrels from strategic reserves—equivalent to roughly two to three weeks of supply in the event of a major disruption.

If disruptions persist then, energy prices could easily past the $118 and push headline inflation higher again. This shifts the inflation outlook from disinflationary demand dynamics toward energy-driven supply pressures.

4. Catalyst and Emerging Divergence

The key catalyst this week—and over the past month—is the Israel–Iran escalation, despite expectations that the conflict may resolve quickly. We could say that as the S&P is still trading within its 2025 – 2026 range.

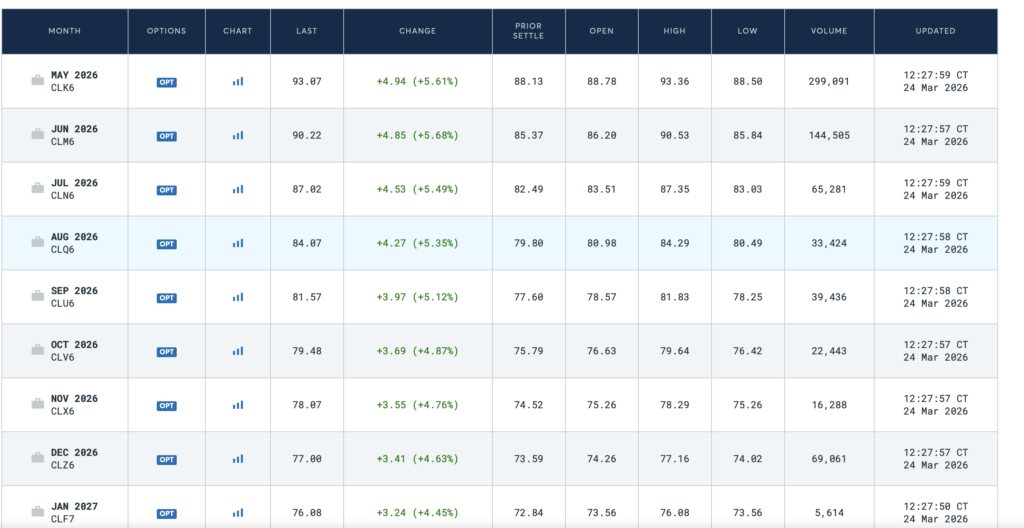

Oil remains around $100/bbl, with geopolitical tensions elevated and limited room for negotiation. The dominant macro risk is a disruption to energy flows through the Strait of Hormuz—something that is not yet fully priced into equities. Oil futures suggest that oil prices will remain elevated, as future prices have increased to around $100 for the rest of the year as noted by Bob Elliott on Twitter. Furthermore, an interesting observation from Warren Pies is that the oil backwardation curve has flattened as longer-dated prices have risen, suggesting that markets expect the supply shock to persist (see below).

Based on the most recent oil futures data as of March 24, 2026 (see chart), the curve is showing flattening backwardation on a significantly higher overall level, with the entire strip jumping roughly 4–5% in a single day. May 2026 is now trading at $93.07.The front end remains steep, with the largest monthly drops concentrated early in the curve (averaging ~$3.00 per month from May to July), while the tail clearly flattens (drops shrinking to ~$1.00 or less per month further out). Today’s gains were also stronger at the front (+$4.94 in May vs. +$3.24 in January 2027). This structure supports Warren Pies’ thesis of persistent near-term supply tightness and suggests that markets now expect the current supply shock to last longer than previously anticipated.

Over the past week, key LNG facilities—including Ras Laffan—have reportedly been destroyed, leading to an immediate tightening in global energy supply. While the damage is not necessarily permanent, repair timelines can extend for months or even years, effectively creating a prolonged supply shock.

G7 reserves could provide only temporary relief (2–3 weeks), leaving markets exposed to a prolonged supply disruption.

At the same time, market pricing has begun to shift.

The short end of the bond market (US 2Y) is at 3.7% (as of March 18, 2026) and closed the week (as of March 22, 2026) at 3.9%, as it is pricing in a higher likelihood of a 15 bps hike this year. Furthermore, both the short and long ends of the Treasury market have erased their earlier gains for the year and are now negative year-to-date.

This suggests the bond market is increasingly pricing higher inflation risk stemming from the energy shock while the equity

5. How the Oil Shock Transmits

There are two key mechanisms through which oil shocks propagate through the economy. While initially inflationary, they tend to become disinflationary or deflationary over time.

Mechanism 1: Demand Compression

Higher energy prices:

- squeeze household budgets

- reduce discretionary consumption

- weaken aggregate demand

Mechanism 2: Financial Conditions and Policy Response

If inflation pressures persist:

- Central Bank hikes / financial condition tightens

- investment slows

- labor markets weaken

Tightening financial conditions reduces consumption, particularly consumption that depends on dissaving or a low-rate environment.

Mechanism 1 and 2 determine how quickly an inflationary shock transitions into a growth shock.

Macro Scenarios

The outcome depends on the starting point of the economy and the policy response.

Scenario 1: Growth Holds Up → Inflation Rises → Central Banks Tighten → Growth Weakens → Faster Cuts

If tightening begins to bite:

• dissaving declines

• consumption weakens

• business activity slows

In this case, deflationary pressures can emerge quickly, and the Fed may eventually cut rates relatively rapidly to stabilize growth.

Scenario 2: Already Weak Economy → Shock Fades → Growth Weakens → Fed Cuts

If consumption and labor markets were already slowing:

• oil acts as an additional tightening force • headline inflation rises temporarily

• but fades quickly as demand weakens

As growth deteriorates, the Fed cuts.

This reduces the need for further tightening. However, if central banks choose to tighten despite weakening growth, the economy could be pushed into a deeper recessionary cycle.

5. Key Insight: Core Inflation Depends on Growth

Research from the Fed supports these macro scenarios and shows that oil shocks pass through to core CPI primarily via macro conditions, rather than directly(see link below).

• strong growth → higher demand → higher core inflation

• weak growth → limited pass-through

While simultaneously, the idiosyncratic shock, effect that energy has on production cost, doesn’t have any impacts on core CPI.

This implies that the inflation outcome depends more on the macro cycle than on the shock itself.

6. Right-Tail Risk: AI Cycle

There is also a right-tail scenario that markets may be underestimating.

If the cycle becomes increasingly driven by AI-related capital expenditure, productivity gains could help absorb some of the inflationary pressure from higher energy prices.

At the same time, the AI cycle could offset demand weakness caused by the energy shock if it leads to entrepreneurial discovery, job creation, and cost reductions—particularly for small and medium-sized enterprises.

Markets appear to assume that AI is both growth-supportive and disinflationary, although whether these productivity gains have already materialized remains uncertain.

7. The Divergence

The key divergence now lies in asset pricing.

• Risk assets (led by Bitcoin): pricing faster Fed easing

• Bonds: pricing higher inflation, a longer Fed hold and increase likelihood of a hike.

The bond sell-off remains orderly, but the divergence is clear—and unresolved.

8. Asset Implications

Bonds

Before the Middle East conflict, the bond market was pricing in a disinflationary growth regime, with Treasuries heavily bid. The short end of the treasury was close to breaking below its 2025 range (see chart 8).

However, the conflict has shifted the macro dynamics. The bond market has begun to price the oil shock as inflationary, pushing out expectations for rate cuts. The US 2-year yield closed the week at 3.68%, while this week it closed at 3.907% (see chart 8 above). Suggesting the market was pricing a prolonged rate hold and now it starts to price a probability of a hike of 15 bps this year. In other words, the bond market is pricing in a higher for longer regime.

Both US 10-year and 2-year Treasuries have reversed their pre-war gains and are now negative year-to-date. Prior to the Iran conflict, the yield curve was undergoing a bull flattening, with the long end declining faster than the short end amid disinflationary growth expectations (see chart 9).

Since the onset of the Iran conflict, the curve has shifted into a bear flattening, with the short end rising faster than the long end. This reflects expectations of tighter monetary policy driven by the oil supply shock.

The key risk for markets is a shift toward bear steepening, where long-term yields rise faster than short-term yields. This would signal that the bond market sees the oil shock as more persistent—an outcome with significant implications for risk assets.

We may already be seeing the early stages of this dynamic, as the yield curve began to bear steepen (see chart 9 above) on Friday amid an escalating conflict that is disrupting critical energy infrastructure and supply across the Middle East.

EUR/USD & FX

Before the Middle East conflict, markets had built significant long EUR positions and crowded short USD trades. The conflict has supported the dollar by creating relative currency pressure on energy-importing economies such as the euro area. An energy shock that disproportionately harms Europe can therefore trigger position unwinds and capital rotation back into the dollar, reinforcing USD strength during the initial phase of the crisis.

In addition, geopolitical disruptions that threaten global energy supply typically trigger risk-off conditions that favor the dollar. Because global oil trade is largely denominated in USD, a sharp rise in oil prices increases global demand for dollars to finance energy purchases. When a shock involves a critical chokepoint such as the Strait of Hormuz—which carries roughly one-fifth of global oil supply—and the destruction of LNG facilities and supplies in the Middle East, this effect becomes even stronger.

Another consideration is that an energy-dependent economy struggling with growth, like the EU, has less wiggle room to remain hawkish without crushing the economy. In this scenario, this would be bearish for EUR. So the fact that ECB officials are showing a willingness to hike on the back of this energy shock is not bullish for EUR.

EUR/USD is now approaching the summer 2025 lows. If the pair breaks below the 1.137–1.139 range, the next downside level around 1.12 becomes possible. From a technical point of view, it is in a daily downturn and is starting a weekly downturn as well (see chart 10). However, for a sustained downturn, we need to see a weekly close below 1.137, followed by a sustained push below 1.12.

Equities

Equities are behaving as if the oil shock will be temporary, yet no commercial tankers are currently willing to pass through the Strait of Hormuz due to security risks, and there is growing doubt that safe passage can be restored quickly.

This creates a clear disconnect: equities remain relatively calm despite recent weakness, leaving them vulnerable to further negative geopolitical developments.

If that pricing of bonds proves correct, the implications are clear: higher real rates would weigh on valuations, while sustained energy prices would compress margins and weaken consumption. Together, these forces point to slower growth and downside risk for equities.

Equities have begun to soften and are now testing 2025 support as the yield curve bear steepens last Friday (see chart 11), but as long as they remain within this range, markets are still effectively pricing earlier Fed easing despite the oil shock.

This creates a conditional setup. If the Fed validates this pricing through signalling earlier easing, equities can stabilize. However, if energy prices remain elevated—particularly above the $118 threshold—demand destruction is likely to emerge, a scenario that is not yet fully priced. In that case, equities would likely need to reprice lower until policy responds.

The key question is whether equities are right to rely on Fed easing and AI-driven growth to offset persistent energy risk—or whether they are underpricing a scenario where demand destruction forces a deeper repricing before policy steps in.

Gold and Crypto

Bitcoin has demonstrated remarkable strength during the oil shock triggered by the US–Israel strikes on Iran, largely due to its positioning as a borderless, non-sovereign hedge against geopolitical uncertainty.

Before the strikes, BTC was trading largely as a proxy for the software sector, which sold off on concerns about AI disruption and rising real yields. Bitcoin’s peak in October 2025 reflected market expectations of liquidity easing that didn’t come through. Despite the Fed’s cuts in September, October, and December, real rates rose, and financial conditions tightened into the new year. At the same time, growth concerns emerged due to AI disruptions and debt-driven capex investment. In that environment, further rate cuts were needed for nominal rates to catch up with cooling inflation, thus lowering real rates.

Following the February 28 strikes, Bitcoin has partially decoupled from the software narrative, performing instead as a geopolitical hedge. The oil shock above $100/bbl introduces deflationary risks by weakening dissaving-driven consumption and softening labor markets. This shifts market focus toward potential earlier Fed easing, allowing BTC to front-run liquidity expectations despite rising nominal yields.

Unlike software stocks tied closely to growth and inflation expectations (with the Nasdaq down roughly 0.5–1%), Bitcoin’s borderless nature has attracted capital flight, including significant outflows from countries affected by the conflict. BTC rebounded to around $76K last monday, acting as a portable safe haven.

Gold, by contrast, has sold off into the US–Israel escalation, pressured by USD strength and rising real yields—behaving less like a safe haven and more like a duration-sensitive risk asset.

Part of this reflects positioning. Gold had become a crowded, leveraged trade, leaving it exposed to liquidations as financial conditions tightened.

At the same time, the oil shock is driving a surge in global dollar demand. In a stress environment, access to funding currencies particularly USD liquidity takes priority over reserve diversification. This raises the risk that some central banks, after years of accumulating gold, may be forced to rotate back into dollars to secure liquidity buffers.

The result is a regime where gold underperforms despite rising geopolitical risk, as dollar scarcity and tighter liquidity conditions dominate traditional safe-haven dynamics. Key risk for Gold is interest rate dynamic, if we see the bonds to start pricing in more cuts for this year, this could be a signal for further leg-up for Gold as it needs to loosen financial condition to thrive.

Final Takeaway

Markets are currently split between two narratives:

- Bonds: inflationary shock + rate hold + increasing probability of a hike

- Risk assets: disinflationary outcome + earlier cuts

The resolution of this divergence will determine the next macro regime.

Thank you for reading!